Understanding Finance, Banking, and Insolvency Disputes in India: A Complete Legal Guide

India’s financial system operates through a regulated framework involving banks, NBFCs, financial institutions, corporate borrowers and individual consumers. Disputes in this sector can significantly affect business continuity, liquidity, creditworthiness and investor confidence. Understanding finance, banking, and insolvency disputes in India is essential because these conflicts impact repayment obligations, asset recovery, restructuring processes and creditor rights India.

Banking disputes India often arise from loan defaults, interest claims, fraud allegations, operational errors or misrepresentation in financial documents. Financial disputes India include disagreements over investments, payment obligations, contract breaches and security enforcement. Insolvency disputes India involve complex procedures under the Insolvency and Bankruptcy Code and usually require proceedings before the National Company Law Tribunal.

This blog explains the categories of disputes, the legal procedures applicable to them, rights of creditors and borrowers, the IBC process India and practical considerations for effective dispute resolution in the finance and banking sector.

1. Nature and Types of Finance, Banking, and Insolvency Disputes

Understanding finance, banking, and insolvency disputes in India begins with recognising the reasons these conflicts arise. Financial relationships involve obligations relating to repayment, security creation, disclosure, compliance and documentation. Disputes occur when parties fail to meet contractual or regulatory expectations.

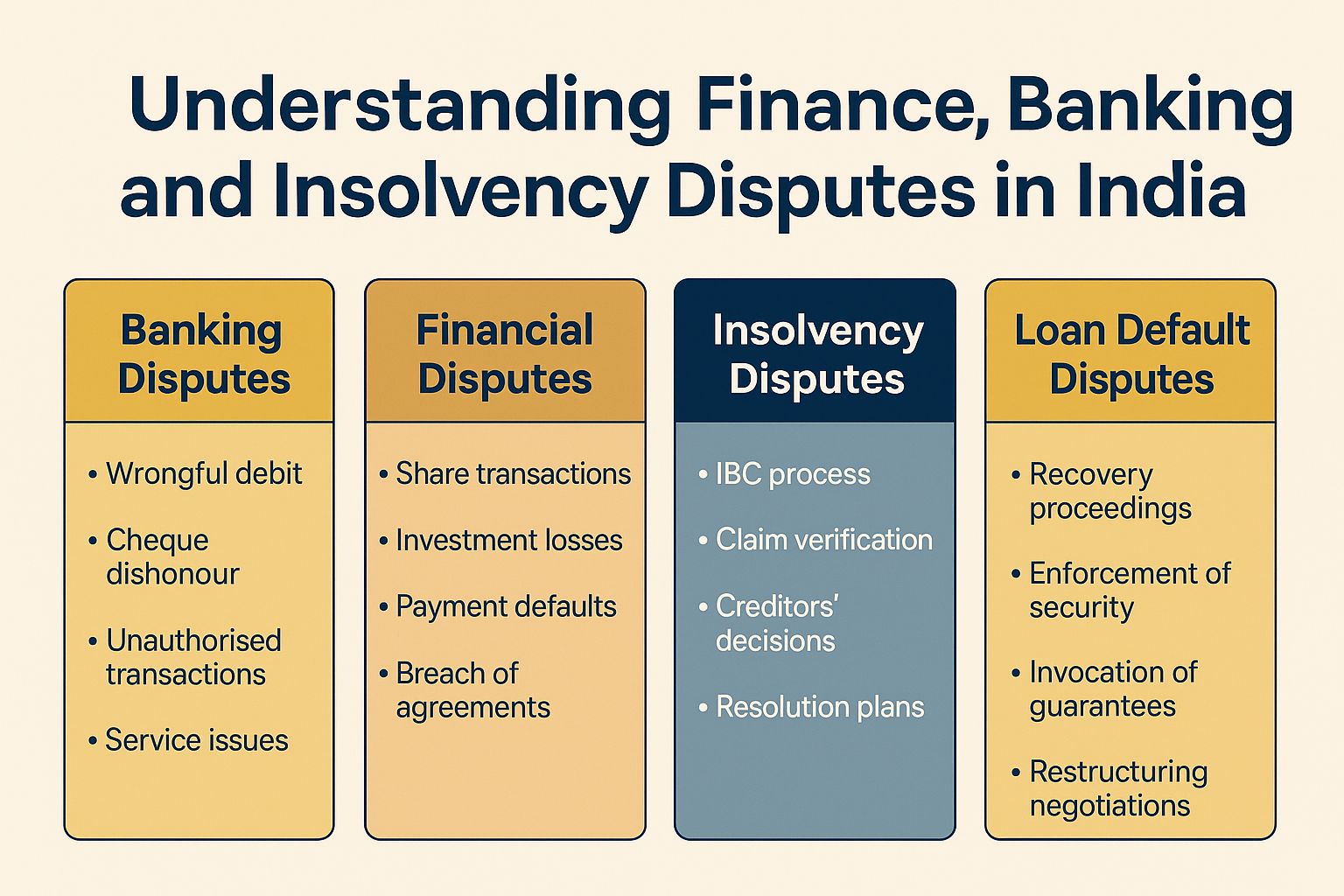

- One major category is banking disputes India, which may involve wrongful debit, cheque dishonour, unauthorised transactions, mis-selling of products, service issues or disputes between customers and banks. Commercial banking disputes also include violations of loan covenants, incorrect classification of NPAs and disputes regarding interest calculations.

- Another major category is financial disputes India, which includes disagreements relating to share transactions, investment losses, non fulfilment of payment terms, misrepresentation in financial statements and breach of funding agreements. Companies engaged in lending or investing face financial disputes due to delayed payments, missed milestones or inaccurate disclosures.

- The most significant category for businesses is insolvency disputes India. These arise when a company defaults on financial or operational dues, triggering the IBC process India. Insolvency disputes involve questions of admission of applications, verification of claims, valuation disagreements, committee of creditors decisions and resolution plan approvals.

- Loan default disputes are also common. These arise when borrowers fail to meet repayment obligations, leading to recovery actions by lenders. Related matters include enforcement of security, invocation of guarantees and restructuring negotiations.

Understanding each category helps businesses and individuals identify the correct legal forum and resolution approach.

2. Legal Framework and Authorities Handling Finance and Banking Disputes

Understanding finance, banking, and insolvency disputes in India requires familiarity with the legal forums and authorities governing them.

- Banking disputes India may be addressed through consumer courts, civil courts or banking ombudsman mechanisms depending on the nature of the issue. Consumer courts handle service-related grievances, while civil courts adjudicate contractual disputes involving large financial claims.

- Loan default disputes and recovery proceedings India are often pursued under special statutes such as the SARFAESI Act, which allows banks to enforce security interests without lengthy court procedures. Lenders may seize assets, auction collateral or take possession of secured properties following statutory notice periods.

- Financial disputes India involving contractual breaches or investment disagreements may be resolved through civil litigation or arbitration depending on the dispute resolution clause in the agreement.

- Insolvency disputes India are handled exclusively by the National Company Law Tribunal (NCLT). Under the IBC process India, creditors or corporate debtors may initiate insolvency proceedings upon default. NCLT disputes India include hearings relating to admission, appointment of resolution professionals, claim verification, valuation approval and plan confirmation.

- Banking fraud complaints may require investigation by specialised agencies. Disputes involving forged documents, fraudulent transfers or diversion of funds may lead to both civil and criminal proceedings.

Understanding the jurisdictional structure ensures that parties choose the correct remedy and forum for dispute resolution.

3. The Insolvency Process and the Role of NCLT in Dispute Resolution

One of the most important aspects of understanding finance, banking, and insolvency disputes in India is the Insolvency and Bankruptcy Code. The IBC introduced strict timelines, creditor control and a transparent restructuring mechanism to handle distressed companies.

The IBC process India begins when a financial or operational creditor files an application before NCLT for initiating corporate insolvency resolution. NCLT reviews whether a default has occurred and admits or rejects the application. Once admitted, a moratorium is imposed on all legal proceedings and recovery actions.

A resolution professional takes control of the company and manages the corporate debtor’s affairs. Creditors submit claims, which are verified and collated. Disputes often arise regarding the classification of claims, admission of amounts and valuation of assets.

The Committee of Creditors plays a central role in insolvency disputes India by voting on resolution plans that determine the future of the distressed company. NCLT disputes India frequently involve challenges to resolution plans, objections by stakeholders, disagreements over fairness and concerns regarding procedural compliance.

If no resolution plan is approved, the company proceeds to liquidation. This leads to asset sales and distribution of proceeds in accordance with statutory priority.

Understanding finance, banking, and insolvency disputes in India requires awareness of these timelines, documentation requirements and the role of creditors in influencing outcomes.

4. Remedies and Resolution Mechanisms for Finance and Banking Disputes

Disputes in the financial sector may involve civil, regulatory or insolvency related remedies. Each category of dispute has distinct methods of resolution.

- For banking disputes India, remedies may include refund of wrongful charges, correction of account statements, compensation for service lapses or restoration of funds in unauthorised transactions. Consumer forums may award compensation or direct banks to take corrective action.

- For financial disputes India, contractual remedies may include damages, specific performance, interest claims or termination of agreements. Arbitration is often preferred in commercial financial disputes.

- Loan default disputes may lead to enforcement of security, attachment of property, sale of collateral or invocation of guarantees. Lenders may also negotiate restructuring arrangements, extend repayment timelines or modify terms to avoid insolvency.

- Recovery proceedings India involve statutory processes under the SARFAESI Act or through debt recovery tribunals. These allow lenders to pursue repayment more efficiently than traditional civil suits.

- For insolvency disputes India, remedies are governed by the IBC. Creditors may seek admission of their claims, challenge undervaluation, contest preferential transactions or oppose approval of certain plans. Borrowers may negotiate restructuring through the resolution process.

- Banking fraud complaints may result in criminal proceedings in addition to recovery actions.

Understanding finance, banking, and insolvency disputes in India enables parties to choose the remedy that best protects financial interests and ensures quicker resolution.

5. Practical Steps for Managing Financial, Banking, and Insolvency Risks

Preventing disputes is as important as resolving them. Understanding finance, banking, and insolvency disputes in India helps businesses adopt preventive measures that reduce risk.

- Organisations should maintain accurate financial records, including repayment schedules, interest calculations, security documents and correspondence with lenders. Clear documentation often prevents dispute escalation.

- Borrowers should ensure timely communication with lenders when facing financial stress. Negotiating restructuring or revised terms at early stages may prevent loan default disputes and avoid insolvency.

- Creditors should conduct thorough due diligence before lending. Monitoring financial performance and compliance with covenants reduces exposure to recovery proceedings India.

- Businesses must understand IT systems to detect unauthorised transactions, manage internal controls and prevent fraud. Banking fraud complaints can be reduced by implementing strong cybersecurity practices.

- Contracts relating to financing, investments or joint ventures should be drafted with clear dispute resolution clauses. Arbitration may be preferred for complex financial disputes India due to confidentiality and speed.

- When facing insolvency disputes India, parties should be well informed about timelines, claim requirements, voting rights and valuation considerations. Working closely with insolvency professionals improves outcomes in NCLT disputes India.

- Understanding digital records, email trails and financial reports also contributes to strong evidence during disputes.

By maintaining transparency, clarity and detailed documentation, both creditors and borrowers can prevent misunderstandings and manage financial risks effectively.

Conclusion

Understanding finance, banking, and insolvency disputes in India is essential for businesses, investors and individuals involved in lending, borrowing or financial transactions. Disputes may involve loan defaults, banking operations, financial disagreements or insolvency matters under the IBC. Effective dispute resolution requires familiarity with legal forums, remedies, creditor rights India and documentation standards.

By adopting preventive measures, ensuring compliance, maintaining clear records and seeking timely professional guidance, parties can manage disputes efficiently and protect financial stability.