Taxation and Financial Regulation Disputes

India’s Goods and Services Tax system is designed to create a unified and transparent framework for indirect taxation. However, because GST is compliance driven and highly structured, disputes between taxpayers and the department are common. Understanding GST disputes is essential for businesses, professionals and service providers because disagreements can arise at any stage of registration, classification, valuation, audit, assessment or input tax credit claims.

GST disputes may involve GST notices India, GST audit issues, departmental inquiries, assessment disagreements, GST penalty disputes and the broader GST litigation process. Resolution requires clarity on legal rights, timelines, jurisdiction and procedures under the law.

This blog provides an in depth explanation of common GST dispute categories, reasons disputes arise, how the GST dispute resolution framework works and best practices to reduce exposure to litigation.

1. Why GST Disputes Arise and How They Impact Businesses

Understanding GST disputes begins with recognising why disagreements occur. GST is compliance intensive. Every business must interpret definitions, rate notifications, exemptions, place of supply rules and input tax credit conditions accurately. Even minor deviations can lead to notices or penalties.

Common triggers include mismatches in returns, short payment of tax, incorrect classification of goods and services or failure to reconcile vendor invoices. Disputes also arise due to delays in filing returns, incorrect reporting of outward supplies and differences between books of accounts and GST returns.

GST departmental inquiries often begin with scrutiny of returns or verification of turnover. These inquiries may escalate into full GST audit issues if officers find inconsistencies. During audits, officers examine purchase registers, sales registers, e way bills, bank statements and agreements. If differences appear unexplained, assessment proceedings may follow.

GST disputes impact cash flow, business continuity and compliance ratings. Non resolution may lead to denial of input tax credit, attachment of bank accounts or prolonged litigation. For these reasons, businesses must understand the root causes and act promptly when disagreements arise.

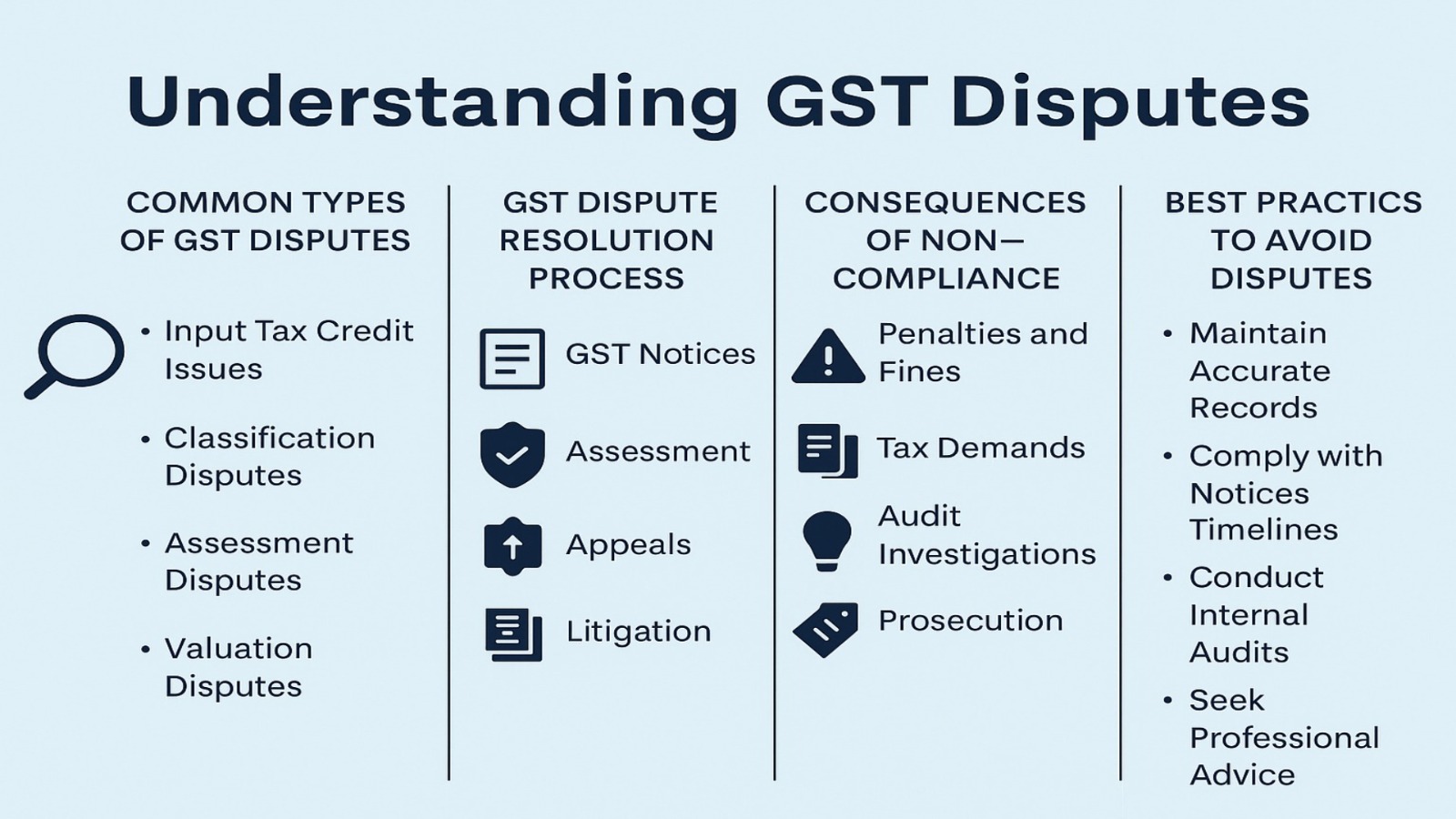

2. Common Types of GST Disputes in India

Understanding GST disputes requires knowing the categories most commonly encountered by businesses.

One of the most frequent issues involves input tax credit disputes. Officers may question the eligibility of credit, claiming that the invoice is defective, the supplier did not file returns or goods were not received. These situations often lead to reversal of ITC and interest demands.

Businesses also face GST notices India relating to classification disputes. Classification determines the applicable tax rate. Misclassification occurs when ambiguous descriptions or complex products are interpreted differently by taxpayers and officers. Classification disagreements directly influence tax liability.

GST assessment disputes arise when officers disagree with reported turnover, taxable value or ITC claims. Officers may issue assessment orders demanding additional tax, interest or penalties. These disputes often require detailed representation and documentary evidence.

Another category involves valuation disputes. Officers may question discounts, reimbursements or composite supplies, claiming that the taxable value does not reflect actual consideration. Businesses must demonstrate how valuation was computed to avoid escalation.

Procedure based disputes also occur frequently. Examples include late filing penalties, mismatched returns, incorrect e way bill details or non compliance with invoice rules. Even minor procedural lapses can create GST compliance issues that lead to formal proceedings.

Understanding this range of disputes helps businesses prepare better documentation and adopt preventive measures.

3. How the GST Dispute Resolution Process Works

The law provides a structured mechanism for resolving disagreements. Understanding GST disputes involves knowing the stages in this mechanism.

The first stage involves receiving a notice. GST notices India may include scrutiny notices, audit notices, demand notices, show cause notices or summons. Each notice has specific timelines and requires a detailed written response supported by documents.

If the officer is satisfied with the reply, the matter may close at this stage. However, if concerns remain, the department may initiate further verification or begin GST assessment disputes. Assessments include provisional assessment, best judgment assessment or summary assessment depending on the circumstances.

If a taxpayer disagrees with the assessment or penalty imposed, they may pursue the GST appeals mechanism. Appeals generally occur before the appellate authority, the appellate tribunal, the high court or the Supreme Court depending on the stage of the dispute. Each stage has strict timelines for filing appeals and producing evidence.

During the GST litigation process, taxpayers must substantiate their position using invoices, reconciliations, agreements, bank statements and statutory records. A complete documentary trail significantly strengthens the taxpayer’s defence.

For certain matters, businesses may seek advance rulings to avoid future disputes. Advance rulings clarify classification, valuation, ITC eligibility or taxability questions. Understanding this system helps taxpayers avoid unnecessary conflict and achieve certainty on legal interpretation.

The dispute resolution framework is designed to offer structure, but businesses must be proactive and organised to achieve favourable outcomes.

4. Consequences of Non Compliance and How Disputes Escalate

Understanding GST disputes also means understanding the consequences of not responding correctly or within the prescribed time. Failure to reply to notices or attend hearings may result in adverse orders, penalties or attachment of property.

GST penalty disputes arise in cases of alleged tax evasion, incorrect reporting, wilful misstatement or procedural lapses. Penalties may include monetary fines along with interest and late fees. In more serious cases, the law allows prosecution for offences such as issuing fake invoices or fraudulently availing ITC.

If a taxpayer does not provide complete records, officers may initiate best judgment assessments. Such assessments often lead to inflated tax demands because they rely on officer estimates rather than factual data.

GST audit issues become more serious when discrepancies force officers to examine multiple years, multiple branches or past transactions. Audits may escalate into detailed investigations if officers suspect deliberate non compliance.

These remedies ensure contract enforceability and help maintain fairness in commercial dealings.

GST departmental inquiries may lead to blocking of input tax credit, suspension of GST registration or restrictions on e way bill generation. These consequences directly affect business operations and supply chains.

To avoid escalation, taxpayers must maintain accurate records, monitor return filing and respond promptly to every communication from the department. Prevention is often more effective than litigation.

5. Best Practices to Avoid and Manage GST Disputes

Businesses can significantly reduce exposure to disputes by following strong internal compliance practices. Understanding GST disputes is not only about resolution but also prevention.

Businesses should maintain complete and accurate documentation including invoices, contracts, delivery challans, ledgers and reconciliations. Periodic reconciliation of GSTR 2B, purchase registers and e way bills helps detect mismatches early.

Regular internal audits ensure that classification, valuation and ITC claims remain compliant. Businesses should review master data, tax rate mapping and transaction flows to identify procedural errors.

Training employees on GST compliance requirements strengthens day to day accuracy. Many disputes arise from simple mistakes in invoice preparation or return filing. Well trained staff reduce these risks.

Responding promptly and professionally to GST notices India helps avoid escalation. Submitting complete documentation builds credibility before the department. Where required, businesses should seek professional assistance to interpret technical issues.

For ongoing GST compliance issues, advance rulings or clarifications help bring certainty. Proper advisory support and legal interpretation prevent future conflicts.

Ultimately, understanding GST disputes and adopting preventive measures ensures that businesses maintain good compliance ratings, avoid penalties and operate without unnecessary disruptions.

Conclusion

Understanding GST disputes is essential for businesses operating in a compliance driven tax system. Disputes may arise from classification errors, ITC disagreements, audit findings or procedural lapses. The GST dispute resolution framework provides structured steps for replying to notices, addressing assessments and pursuing appeals where necessary.

By strengthening documentation, improving internal controls and responding promptly to departmental inquiries, businesses can minimise the risk of litigation and maintain seamless compliance. A strong understanding of GST audit issues, GST notices India and penalty provisions ensures businesses stay protected and operate with confidence in a complex regulatory environment.